We believe that we are reaching an inflection point in markets where the economic market structure that has existed since the Great Financial Crisis (GFC), with prolonged business cycles driven by government intervention and mispriced risk, is running out of steam. We believe this to be an opportunity for active management, underpinned by fundamental and sustainable investment research, to return to the forefront.

Whilst some market participants believe that a second Trump presidency may lead to better economic outcomes and an elongation of the current business cycle, we would argue that the world ahead will likely be one with increased volatility and uncertainty on the back of trade, fiscal, immigration, and regulatory policy. We cannot remember a time in our careers when the range of our economic outlook and scenarios, as we think about a twelve-month period ahead, have been so wide-ranging.

Economic Outlook Scenarios 2025 And Beyond

U.S. policy is creating a high degree of uncertainty for global fixed income markets in 2025 and beyond. Whilst we don’t believe that our base case scenario has materially changed, we have assigned the lowest probability to a central scenario in our 15 years of doing this together as a team. Our base case calls for moderate growth with the U.S. continuing to outperform the rest of the developed world, and a continuation of the disinflationary process that has been evident over the past two and a half years. We believe that monetary policy and financial conditions are still tight and that central banks will continue to ease policy to a more neutral stance. The resilience of labour markets post-pandemic, and particularly in the U.S., has enhanced stability and averted an outright global recession. In our view, the appreciation of home prices and equities have supported consumption over this period. The performance of asset prices will be an important determinant as to whether this current phase of the economic cycle can continue through 2025.

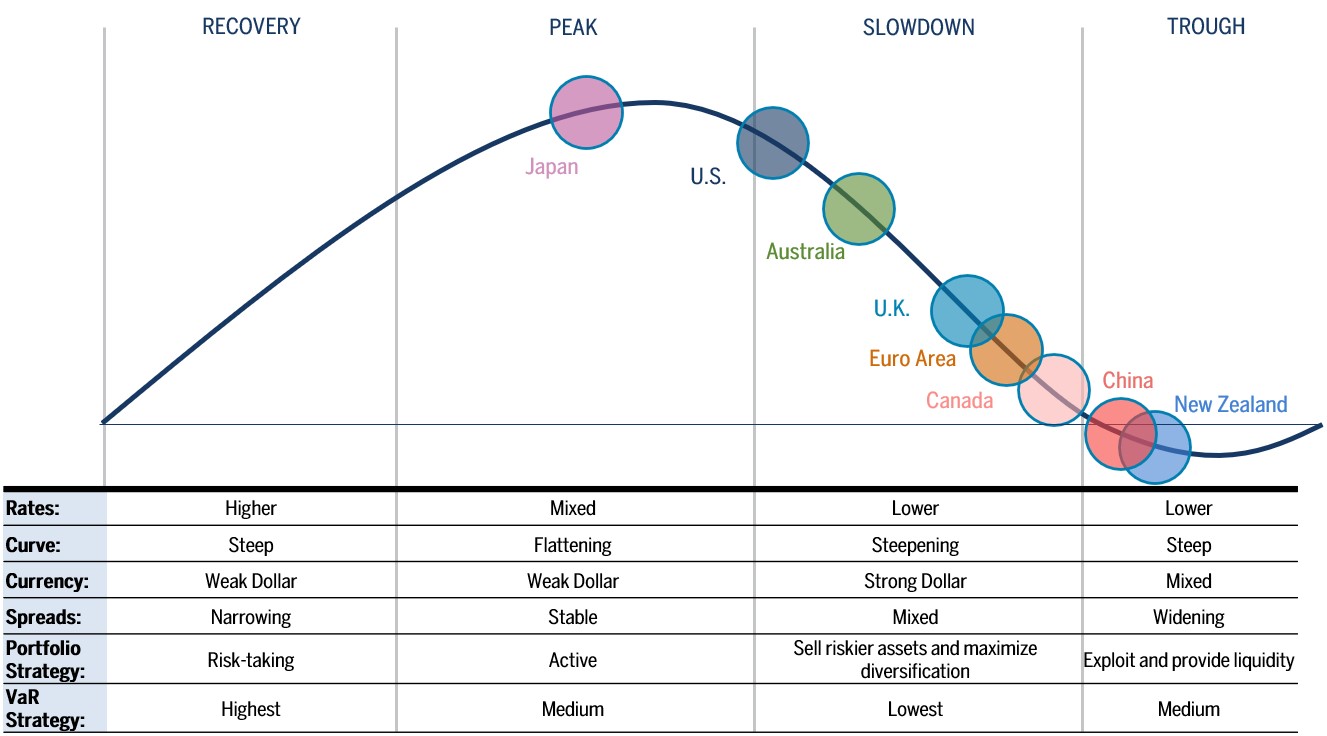

We expect the U.S. to see better economic performance coupled with ever-expanding deficits thus limiting a decline in longer-term interest rates. On the other hand, we continue to see a weaker economic picture in countries such as Canada, New Zealand, and within Europe. While we expect international markets to grow below trend, the threat of U.S. tariffs, either directly or indirectly, adds further downside risk to growth, driving down inflation and leading to further and significant monetary easing in 2025, albeit at a slower pace than in the previous year. Japan remains the exception to this trend in developed market economies as the Bank of Japan, in our view, will continue to raise interest rates to slow upward pressure in wages and inflation.

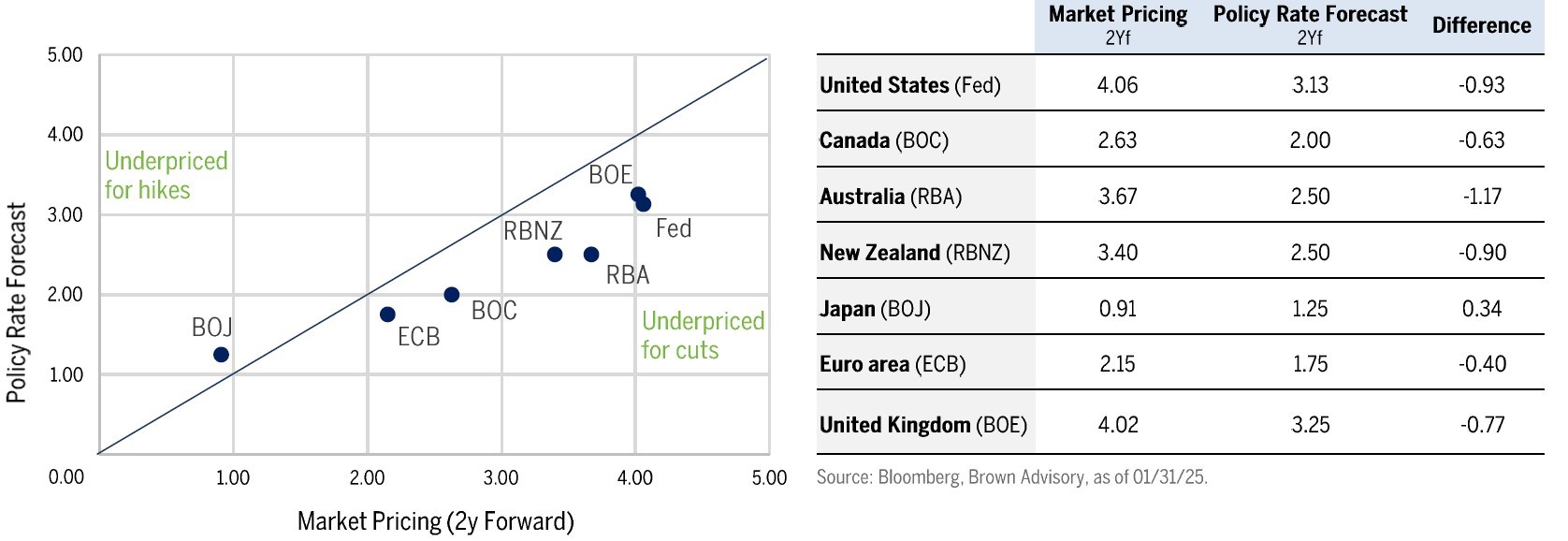

CENTRAL BANK FORECASTS VS MARKET

Source: Brown Advisory, as of 12/31/2024.

In such a scenario emerging market (EM) countries would be challenged by the uncertainty associated with U.S. trade policy. Weakening local currencies and bloated debt levels could severely limit financial and economic flexibility in the emerging world.

In our annual scenario forecasting, we have increased the probabilities assigned to negative tail-risks to the global economy. What is different this year, perhaps, is that we can envision two distinct negative outcomes: the first, a more traditional economic slowdown which is accompanied by slowing inflation; the second, a stagflationary environment that includes weaker growth with higher inflation as a result of tariffs and supply chain disruptions. Both would result in risk markets underperforming, but the implications for central bank policy and interest rates would be markedly different.

In the first negative scenario, we would expect to see aggressive central bank easing on the back of materially weaker growth and inflation. As unemployment rises and consumption weakens, overnight rates will have to move below neutral in order to stimulate economies. In a stagflationary environment, similar to 2022, interest rates would have to remain high in order to offset the inflationary pressures caused by higher tariffs alongside fiscal expansion. This is the environment – whilst less likely, in our view, than a traditional economic slowdown – that concerns us the most.

“As we manage assets in an asymmetric asset class that has limited upside and where downside can be zero, we need to constantly be focused on protecting our clients’ capital by constructing portfolios that can not only deliver performance in positive markets but be an important counterbalance to equity risk in more challenging times.”

Ryan Myerberg, Global Sustainable Fixed Income Portfolio Manager

Investment Implications And Positioning

We maintain the core view that positioning for steeper yield curves will be effective in both a growth slowdown and a fiscally expansionary environment. As such, the portfolio has concentrated duration positions in short to intermediate maturities across the developed world. We believe that the Fed will continue to ease monetary policy, and that term premium further out the yield curve is too low. We also generally favour other developed-world duration outside the U.S., such as Canada, New Zealand, Australia, and Europe. We’ve long suggested that the post-GFC environment of stubbornly harmonized economic and fiscal/monetary cycles is over, and we’re seeing clearer signs of divergences in the economic outlooks for countries around the world. We believe that 2025 will provide compelling levels to add to countries and regions where rate cuts continue to be likely and necessary.

Our strategy is dynamic and unconstrained by a benchmark and looks to generate attractive risk-adjusted returns through an economic cycle with positive sustainability outcomes. This allows us to dynamically allocate risk between a broad set of asset classes and geographies. Based on our economic cycle assessment we expect most returns to be driven in 2025 by our rates positioning whilst we wait for better opportunities to increase our exposure to corporate credit. We see a deterioration of fundamentals, driven by weaker revenue, higher cost of capital and lower pricing power affecting margins and profits. At the same time, we continue to see credit spreads as expensive, making the asset class relatively less attractive. In this environment we prefer high quality credit and have focused on optimizing our existing positions for yield as well as building out a ready-to-buy list in corporate credit with the anticipation of having attractive entry points in 2025.

CYCLE ASSESSMENT FOR MAJOR ECONOMIES

Source: Brown Advisory, as of 12/31/2024.

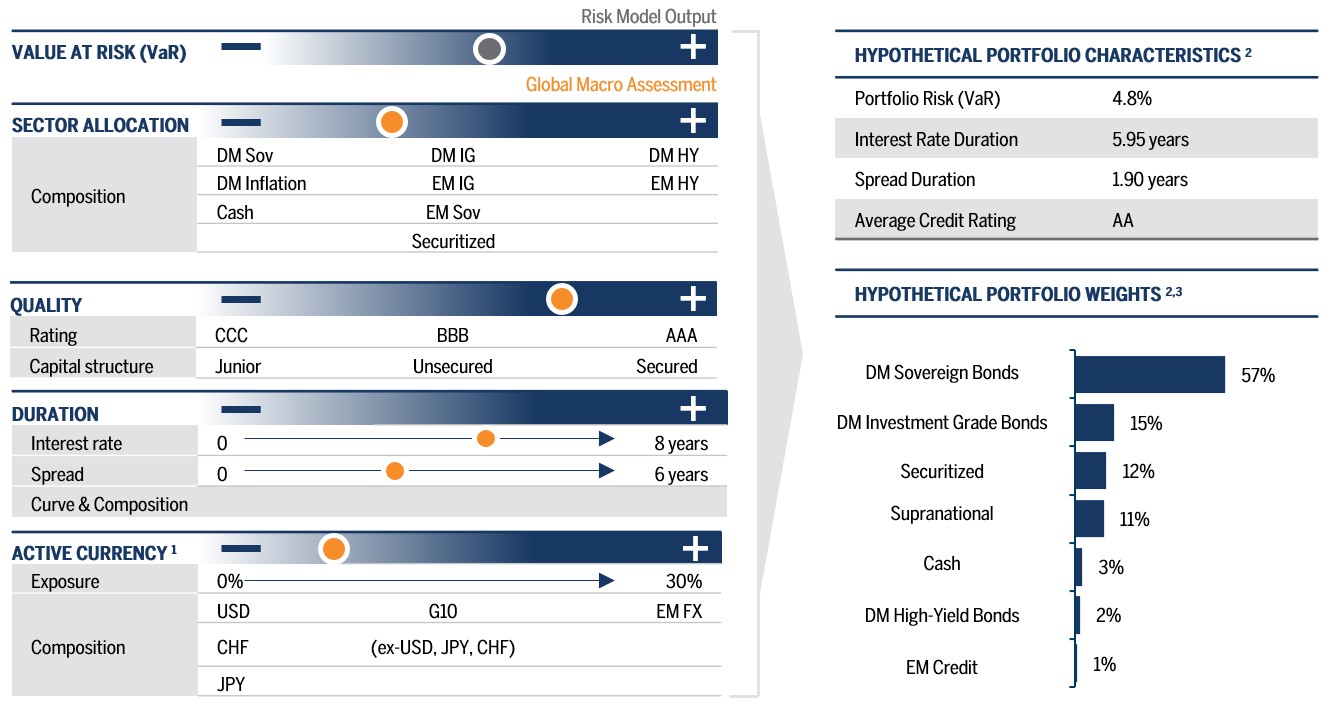

A FRAMEWORK FOR DYNAMIC ASSET ALLOCATION 2

Source: Brown Advisory, as of 12/31/2024.

1. Currency exposure resulting from an allocation to bonds is fully hedged. Currency exposure in the portfolio is an active decision.

2. Based on a hypothetical asset allocation, does not represent an actual client’s investments and is intended for illustrative purposes only.

3. Sum of portfolio weights is more than 100% as the chart does not include futures used to hedge duration exposure. Please see the end of the presentation for important disclosures.

Three Years Of The Brown Advisory Global Sustainable Total Return Bond Strategy

This year marks the strategy’s third anniversary. From a performance perspective, the Brown Advisory Global Sustainable Total Return Bond strategy has outperformed many of its peers during its three-year lifespan and exhibited strong downside capture and maximum drawdown management over that time. Its total return of 2.0% is 3.9% above the performance of the main Bloomberg Global Aggregate Bond Net Index.1 This performance was achieved during a time when challenging market conditions have often warranted a more cautious stance, and we have prioritized downside protection ahead of chasing the upside. The heart of our investment approach has always been to offer clients two core deliverables: attractive risk-adjusted returns over the course of an economic cycle, as well as the preservation of capital, especially during challenging market environments. To us, these goals are the foundation of our investment philosophy, which has been formulated over nearly 15 years of working together and informs our strategic and flexible approach to navigating markets. Past success doesn’t mean we will now rest on our laurels. We constantly strive to be better and ensure our process can adjust to changing market conditions. We are confident that our strategy will continue to be able to capture future opportunities, avoid downside risk and deliver sustainability outcomes for the next three years and beyond.

PORTFOLIO MANAGERS, GLOBAL SUSTAINABLE TOTAL RETURN BOND STRATEGY

Chris Diaz, CFA

Portfolio Manager

Ryan Myerberg

Portfolio Manager

Colby Stilson

Portfolio Manager

1. Source: Factset®, as of 12/31/24.

Disclosures

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested.

The Global Sustainable Total Return Bond Fund is a UCITS fund and is available to U.S. investors.

The composite performance shown above reflects the Global Sustainable Total Return Bond Composite, managed by Brown Advisory Institutional. Brown Advisory Institutional is a GIPS compliant firm and is a division of Brown Advisory LLC. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. Please see the Brown Advisory Global Sustainable Total Return Bond Composite disclosure statement at the end of this document for a GIPS Report.

The portfolio information provided is based on the Brown Advisory Global Sustainable Total Return Bond (GBP) Representative Account as of 12/31/2024 and is provided as Supplemental Information. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities or funds mentioned. It should not be assumed that investments in such securities or funds have been or will be profitable. Please see disclosure statements at the end of this presentation for additional information and a complete list of terms and definitions.

The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities or issuers mentioned. It should not be assumed that investments in such securities or issuers have been or will be profitable. References to specific securities or issuers are to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy and is not a complete summary or statement of all available data.

Sustainable investment considerations are one of multiple informational inputs into the investment process, alongside data on traditional financial factors, and so are not the sole driver of decision-making. Sustainable investment analysis may not be performed for every holding in evert strategy. Sustainable investment considerations that are material will vary by investment style, sector/industry, market trends and client objectives. Certain strategies seek to identify companies that we believe may be desirable based on our analysis of sustainable investment related risks and opportunities, but investors may differ in their views. As a result, these strategies may invest in companies that do not reflect the beliefs and values of any particular investor. Certain strategies may also invest in companies that would otherwise be excluded from other funds that focus on sustainable investment risks. Security selection will be impacted by the combined focus on sustainable investment research assessments and fundamental research assessments including the return forecasts. These strategies incorporate data from third parties in its research process but do not make investment decisions based on third-party data alone.

Bloomberg Global Aggregate Index (1-10Y) (GBP Hedged) represents a close estimation of the performance that can be achieved by hedging the currency exposure of its parent index, the Bloomberg Global Aggregate Bond Index, to GBP. The index is 100% hedged to the GBP by selling the forwards of all the currencies in the parent index at the one-month Forward rate. The parent index is composed of government, government-related and corporate bonds, as well as asset-backed, mortgage-backed and commercial mortgage-backed securities from both developed and emerging markets issuers.

Bloomberg Global Aggregate Net Index (GBP Hedged) measure of global investment grade debt from twenty-eight local currency markets. Bloomberg Indexes and its associated data, Copyright ©2022 Bloomberg Index Services Limited. Bloomberg® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Bloomberg does not approve or endorse this material or guarantee the accuracy or completeness of any information herein, nor does Bloomberg make any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, Bloomberg shall not have any liability or responsibility for injury or damages arising in connection therewith.

Duration is a time measure of a bond’s interest-rate sensitivity, based on the weighted average of the time periods over which a bond’s cash flows accrue to the bondholder.

Volatility is the degree of variation of a trading price series over time, usually measured by the standard deviation of returns.