“It is not the most intellectual of the species that survives; it is not the strongest that survives; the species that survives is the one that is able best to adapt and adjust to the changing environment in which it finds itself.”

– Charles Darwin

The first half of this decade has not proven to be an easy environment for fixed income investors.

It has marked a major inflection point for the global macroeconomic landscape, which has transitioned from the post-Global Financial Crisis (GFC) landscape into a new paradigm of higher inflation and interest rates, fiscal consolidation rather than expansion, deglobalization amid geopolitical tensions and increased market volatility. At the same time, the rising implications and costs of climate change, a heightened focus on energy security and the transition away from carbon-based power sources and increasing social tensions have added to the array of investor challenges.

Given this has been such a challenging juncture for our asset class, we are often asked why we chose to launch our Brown Advisory Global Sustainable Total Return Bond Strategy in 2022.

The strategy’s third anniversary marks the perfect time to reflect on this decision and assess our performance so far. Whilst we acknowledge that the last three years may have accelerated our ageing process, we firmly believe there has been no better time to demonstrate proof of concept that our investment philosophy and process are equipped to deliver during turbulent periods. And it is important to acknowledge that as well as challenges, change also creates new or differing opportunities.

Our experience in managing fixed income assets has taught us that you mustn’t resist change. As Charles Darwin states, survivors ‘adapt and adjust to the changing environment’. For us, this means not just positioning our portfolios for today but being strategic and flexible in building portfolios that are fit for an ever-altering future.

Keeping An Eye On The Future

The heart of our investment approach has always been to offer clients two core deliverables: attractive risk-adjusted returns over the course of an economic cycle, as well as the preservation of capital, especially during challenging market environments. To us, these goals are the foundation of our investment philosophy, which has been formulated over nearly 15 years of working together and informs our strategic and flexible approach to navigating markets.

First and foremost, we believe it is essential to recognise that the world is constantly changing. Rather than being dogmatic and expecting markets to always suit one style of investing, we take our lead from Darwin and focus on evolution. This starts with not only assessing where the macroeconomic environment is today, but how it may shift over the next two, three and four years, and selecting the most suitable assets to maximize those opportunities.

This focus on the future gives us the ability to better gauge valuations throughout a changing cycle and provides us with more favorable odds for asset allocation decision-making. With this pliable mindset, we are not only able to participate in market upside but believe we can also manage downside risk, thereby creating an asymmetric payoff which results in a smoother return profile.

In the first negative scenario, we would expect to see aggressive central bank easing on the back of materially weaker growth and inflation. As unemployment rises and consumption weakens, overnight rates will have to move below neutral in order to stimulate economies. In a stagflationary environment, similar to 2022, interest rates would have to remain high in order to offset the inflationary pressures caused by higher tariffs alongside fiscal expansion. This is the environment – whilst less likely, in our view, than a traditional economic slowdown – that concerns us the most.

A More Sustainable World

In our view, having an eye on the future also involves incorporating sustainability considerations into our investment process. As the world progresses, albeit slowly, in the fight against climate change, the need to better protect and conserve nature, improve labour and social practices, and ensure appropriate governance standards, we see sustainability and economic factors becoming ever more closely intertwined.

Therefore, it seems natural to us that our research approach not only reviews the world through a fundamental, economic lens, but also applies a sustainability lens as well. This ‘bi-focal’ view deepens our ability to understand the opportunity and risk within our investment universe, which we believe will be accretive in the context of our longer-term performance.

For example, we believe that identifying those countries and companies that are doing the best job of integrating sustainability concepts into their economic and business models, thereby improving their opportunities and mitigating the associated risks, will be future outperformers.

Our focus on sustainability can also enhance downside risk management, by helping us avoid upcoming risks. Since the strategy’s inception, there have been several instances where risks were flagged by our sustainability risk assessments in certain sovereigns or companies, prompting us to stay clear from these investments that later faced times of crisis: Russian sovereign debt in 2022, or Credit Suisse bonds in the spring of 2023, to name two examples.

But identifying the risks and opportunities surrounding sustainability is not solely about enhancing performance; we take pride in knowing that – unlike many of our peers – the investments we make are also aligned with positive environmental and social outcomes. For example, we’ve invested in India Green Power, a 100% renewable energy provider which is playing a key role in reducing India’s CO2 emissions, 40% of which comes from the power sector. Not only has that bond provided a 19.25% total return for our investors since we initiated the position in the strategy, but it has also provided funding to a company that we believe is making a significant contribution to the green energy transition in India in order to help meet the country’s ambition to achieve Net-Zero by 2070.1

Balancing The Top-Down / Bottom-Up Equation

The formation of our macroeconomic views also helps our strategy stand out. We strongly believe that top-down factors such as duration, curve and asset allocation are the dominant drivers of risk and returns for this asset class. However, we reinforce this top-down analysis with additional inputs from our bottom-up research across sovereigns, corporates and securitized issuers. Our analysts regularly share the forward-thinking intel gained from company and country research, which gives our forecasting process an edge in determining future macro and market trends and ultimately informs our portfolio construction decisions.

As an example, the publicly available data on labour markets and sentiment can be complemented by the direct information we receive from companies about capital expenditure and hiring decisions to provide a better real-time indicator of where the economic cycle is going.

Our dual approach certainly proved to be efficient in 2022, when central banks were cautioning that higher inflation would only be transitory, whereas companies were anecdotally discussing the hoarding of labour and their inability to hire. These conflicting signals informed our decision to position the portfolio for a more resilient high-inflation environment combined with a demand slowdown.

The intersection between top-down and bottom-up can inform our sustainability perspective too. Macro data and studies have shown that climate risk is going to have an increasingly financially material impact on certain businesses, but the bottom-up, credit-focused engagement with the companies and governments in which we invest helps us better understand not only the specific risks they are facing, but also what are they doing to tackle these risks.

An Eye On The Past

Even though our approach is firmly aligned with the future, we often look to the past for a reference on macro trends or market patterns. Right now, we believe the post-Covid economic and market structure is transitioning back to themes that are reminiscent of the pre-GFC world. An economic regime that was characterized by increased volatility along with higher interest rates, inflationary pressures and reduced government intervention; and a market landscape where credit default cycles had higher peaks and average default rates than in the post-GFC era.

The ability to recognise and learn from past economic and market phases is particularly crucial for portfolio construction, as they can help inform appropriate risk levels and compositions.

One of our key commitments to our clients is to ensure that our economic views and portfolio positioning will be aligned, aiming to minimize surprises for our clients when comparing expectations versus outcomes. This seems simple, but it is surprising how often portfolios can become out of sync.

We have observed that since the GFC, fixed income as an asset class has become less and less liquid. While it is still possible to reposition risk, doing this at speed and scale is not always straightforward. Therefore, we believe our combined focus on strategizing for the future alongside leveraging the past for guidance helps ensure our portfolio remains positioned for where economies and markets are heading tomorrow rather than where they were yesterday.

Going Anywhere

Our multi-faceted macro lens helps us to maximize the strategy’s ‘go-anywhere’ potential. Throughout an economic cycle, there are always differing opportunities – be they idiosyncratic, geographic or across asset classes. Our remit gives us the latitude to cast our net wide and take advantage of the available opportunities. We’ve used a significant amount of our interest rate flexibility over the past three years, found alpha opportunities in the currency markets, whether by being structurally long the US dollar in 2022 or via relative value trades within the dollar bloc or emerging markets or, more recently, shifted our geographic exposure in sovereigns significantly away from the United States towards countries where we believe trade, tariff, and growth uncertainties and downside risks will provide significant total and excess returns.

Our macro insights also signal when it’s time to put risk on or take it off the table. The combination of monitoring different phases of the cycle and having the flexibility to react – ideally ahead of periods of market stress – have helped us achieve a relatively smooth delivery of capital returns. Notably, the strategy’s low duration and credit exposure in 2022 provided downside protection during a period of high market volatility with a maximum drawdown that was 6.45% less than the Bloomberg Global Aggregate Bond Index and 6.74% less than the average of our peer group.2

The flexibility of our strategy is epitomised by our benchmark agnostic stance. Our long experience of working as a team has made us wary of the embedded risks that come with managing to a benchmark. These risks could come in the form of too much interest rate duration, or exposure to risk assets at the wrong time in the cycle. We have found that trusting our macroeconomic insights alongside our bottom-up research enables us to construct robust fixed income portfolios that have the ability to perform in almost any market environment.

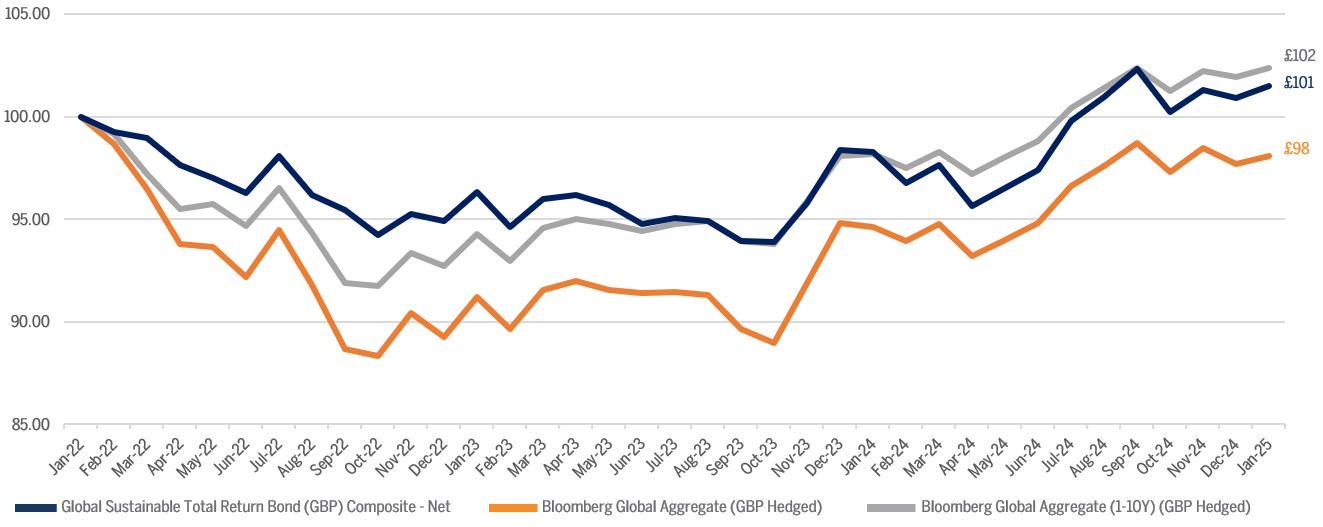

CUMULATIVE RETURNS

Source: Growth of £100 (net of fees) from inception to January 31, 2025

Source: Source: FactSet, as of 01/31/25. All returns greater than one year are annualized. Past performance is not indicative of future results. The Composite inception date is February 1, 2022.

Continuous Adaptation

When you reach any milestone, it’s natural to look back on what you have achieved and how you have achieved it. From a performance perspective, the Brown Advisory Global Sustainable Total Return Bond Strategy has outperformed many of its peers during its three-year lifespan and exhibited strong downside capture and maximum drawdown management over that time. Since inception, its total net return of 2.0% is 3.9% above the performance of the main Bloomberg Global Aggregate Bond Index – performance achieved during a time when challenging market conditions have often warranted a more cautious stance, and we have prioritised downside protection ahead of chasing the upside.3 We’re proud of our information ratio, a key measure of performance, that shows our ability to deliver on our stated objective of risk-adjusted returns for our investors.

Yet, this is not just a three-year journey. Our story harks back to 2011 when we first began working together. The longevity of this relationship means that the integrity of our investment process has been tested through different market phases – and verified by our top-decile prior track record. We have found that what initially united us, and reunited us at Brown Advisory, is our shared belief in the investment outcomes we want to achieve and having the complementary skillset that enables us to do just that.

And past success doesn’t mean we will now rest on our laurels. We constantly strive to be better and ensure our process can adjust to changing market conditions. Building on Darwin’s theory of evolution, our process of continuous adaptation means we believe our strategy will be well-positioned to capture future opportunities, avoid downside risk and deliver sustainability outcomes for the next three years and further on.

We thank our investors for their early support and look forward to seeing you soon.

PORTFOLIO MANAGERS, GLOBAL SUSTAINABLE TOTAL RETURN BOND STRATEGY

Chris Diaz, CFA

Portfolio Manager

Ryan Myerberg

Portfolio Manager

Colby Stilson

Portfolio Manager

1. Company Reports, Brown Advisory Analysis, as of 12/31/2024.

2. Source: Morningstar, as of 12/31/2024.

3. Source: FactSet®, as of 12/31/2024. All returns greater than one year are annualized. Past performance is not indicative of future results.

Unless otherwise stated, sources are as of the most recent company reports available at the time of publication. All financial statistics and ratios are calculated using information from Factset as of the report date unless otherwise noted.

Past performance is not indicative of future results and you may not get back the amount invested. The benchmark is the SONIA (Sterling Overnight Index Average) Index of very short-term unsecured loans between U.K. financial institutions. Secondary benchmarks are the Bloomberg Global Aggregate Index (1-10Y) (GBP Hedged) and Bloomberg Global Aggregate (GBP Hedged). The composite performance shown above reflects the Global Sustainable Total Return Bond GBP composite, managed by Brown Advisory Institutional. Brown Advisory Institutional is a GIPS Compliant firm and is a division of Brown Advisory LLC. Please see the Brown Advisory Global Sustainable Total Return Bond GBP composite disclosure statement at the end of this presentation for a GIPS Report. The Composite inception date is February 1, 2022.

Disclosures

The views expressed are those of the author and Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested.

The composite performance shown above reflects the Global Sustainable Total Return Bond Composite, managed by Brown Advisory Institutional. Brown Advisory Institutional is a GIPS compliant firm and is a division of Brown Advisory LLC. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. Please see the Brown Advisory Global Sustainable Total Return Bond Composite disclosure statement at the end of this document for a GIPS Report.

The portfolio information provided is based on the Brown Advisory Global Sustainable Total Return Bond (GBP) Representative Account as of 12/31/2024 and is provided as Supplemental Information. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities or funds mentioned. It should not be assumed that investments in such securities or funds have been or will be profitable. Please see disclosure statements at the end of this presentation for additional information and a complete list of terms and definitions.

The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities or issuers mentioned. It should not be assumed that investments in such securities or issuers have been or will be profitable. References to specific securities or issuers are to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy and is not a complete summary or statement of all available data.

Sustainable investment considerations are one of multiple informational inputs into the investment process, alongside data on traditional financial factors, and so are not the sole driver of decision-making. Sustainable investment analysis may not be performed for every holding in evert strategy. Sustainable investment considerations that are material will vary by investment style, sector/industry, market trends and client objectives. Certain strategies seek to identify companies that we believe may be desirable based on our analysis of sustainable investment related risks and opportunities, but investors may differ in their views. As a result, these strategies may invest in companies that do not reflect the beliefs and values of any particular investor. Certain strategies may also invest in companies that would otherwise be excluded from other funds that focus on sustainable investment risks. Security selection will be impacted by the combined focus on sustainable investment research assessments and fundamental research assessments including the return forecasts. These strategies incorporate data from third parties in its research process but do not make investment decisions based on third-party data alone.

Bloomberg Global Aggregate Index (1-10Y) (GBP Hedged) represents a close estimation of the performance that can be achieved by hedging the currency exposure of its parent index, the Bloomberg Global Aggregate Bond Index, to GBP. The index is 100% hedged to the GBP by selling the forwards of all the currencies in the parent index at the one-month Forward rate. The parent index is composed of government, government-related and corporate bonds, as well as asset-backed, mortgage-backed and commercial mortgage-backed securities from both developed and emerging markets issuers.

Bloomberg Global Aggregate Net Index (GBP Hedged) measure of global investment grade debt from twenty-eight local currency markets. Bloomberg Indexes and its associated data, Copyright ©2022 Bloomberg Index Services Limited. Bloomberg® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Bloomberg does not approve or endorse this material or guarantee the accuracy or completeness of any information herein, nor does Bloomberg make any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, Bloomberg shall not have any liability or responsibility for injury or damages arising in connection therewith.

Duration is a time measure of a bond’s interest-rate sensitivity, based on the weighted average of the time periods over which a bond’s cash flows accrue to the bondholder.

Volatility is the degree of variation of a trading price series over time, usually measured by the standard deviation of returns.

Information Ratio is the measure of the risk-adjusted return of a portfolio defined as expected active return divided by tracking error, where active return is the difference between the return of the portfolio and the return of a selected benchmark index, and tracking error is the standard deviation of the active return.