Our Large-Cap Sustainable Growth portfolio managers discuss how they have approached the health care sector as sustainable investors.

Some of the most compelling investments over the next decades, in our view, will be in companies that help solve some of society’s thorniest challenges—resource scarcity, chronic health crises, access to clean water and climate change, to name a few. Companies that do this exceptionally well can often put themselves in position to generate robust growth and profitability and reward shareholders over the long term.

Our entire portfolio is built on this philosophy. Our investment criteria have led us to find these solution providers across a variety of sectors, particularly among health care, industrial and information technology companies. It turns out that companies can, in fact, often generate strong business results through products and business approaches that reduce energy and resource consumption, improve health outcomes, mitigate carbon emissions, and offer solutions to our long-term sustainability challenges. Our portfolio’s emphasis on these companies—and our willingness to decouple from our benchmark’s sector makeup to own sizable positions in them—has been a primary driver of our returns since inception.

In this article, we will focus on our strategy’s health care investments, which have generated a 19% annualized return over the past five years ended Sep. 30, 2019, compared to a comparable figure of 8% for the health care holdings in our benchmark, the Russell 1000® Growth Index. Combined with a fairly consistent overweight in the sector over time, our stock selection in health care has driven an outsized proportion of our relative outperformance during that period.

Here we discuss what attracts our interest in the sector, and what drives us away—and show how our choices have impacted our divergence of returns vs. our benchmark.

SECTOR BACKDROP

The importance of the health care sector to both society and the global economy is undeniable. Global health care spending is likely to exceed $10 trillion per year by 2022, according to Deloitte’s 2019 Global Health Care Outlook. Unsurprisingly, health care has also grown to become the second-largest sector in public equity markets, representing 13.7% of the market cap of the S&P 500 Index as of Aug. 31, 2019.

The sector is making meaningful strides—notably, in the global fight against communicable diseases, and in innovative biotechnology research that offers hope for curing cancer, rare diseases, and other previously unsolvable medical challenges.

Intractable challenges and obstacles remain: rising (some would say runaway) costs, rapid changes to the models used to deliver care, impacts from climate change and pollution, and massive inequities in access to care. Better health care data comes with the challenge of keeping that data private and secure. Drug pricing is a well-documented issue and few, if any, answers will satisfy all stakeholders. And the regulatory risks facing pharma and biotech companies are often binary in nature—FDA approval can mean billions in revenue, while a failed trial can lead to bankruptcy.

The sector, therefore, presents fertile ground for investors but also contains plenty of danger. Our investment philosophy has always been to start with fundamentally strong companies that we believe are employing smart sustainability strategies to manage their risks, improve their cost structures, and create opportunities for long-term growth. Our approach in health care is no different.

A DRILLDOWN ON OUR PORTFOLIO

We generally focus our investments on solutions that we believe can achieve measurable and reliable results. We prefer businesses that have some control over their own destiny. In health care, these companies often include devices, services, tools or technologies that generate consistent results for customers such as shorter hospital stays for patients, reduced medical waste, higher success rates for medical procedures, or other tangible and (somewhat) predictable outcomes.

We try to avoid companies that, in our view, are excessively exposed to pressures out of their control. In the health care sector, material shareholder value is too often subject to any number of surprises including clinical trial failures, political rhetoric around private/public health insurance, and drug pricing scrutiny. Price volatility is often triggered by these issues, and we find it difficult to justify sizable investments in firms tied to this volatility. We therefore seek to minimize exposure to these issues. (We can’t always avoid these issues entirely, however—for example, portfolio holding UnitedHealth is a well-positioned provider in our view, but it is nonetheless tied to the ongoing debate about universal health care and the potential elimination of private health insurance.)

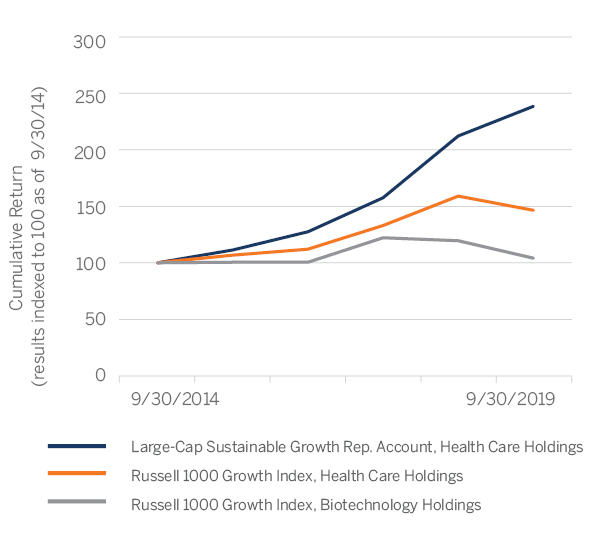

Selected Sector Returns (Gross) Large-Cap Sustainable Growth Rep. Account vs. Russell 1000 Growth Index 9/30/2014–9/30/2019 (Index=100)

Source: Bloomberg. The portfolio information provided is based on a representative Large-Cap Sustainable Growth account and is provided as supplemental information. Sector allocations exclude cash and cash equivalents. Sectors and subsectors are based on the Global Industry Classification Standard (GICS®) classification system. Please see disclosure statements at the end of this presentation for the complete Large-Cap Sustainable Growth GIPS-compliant disclosure.

The table below shows how our “basket” of health care holdings has performed over the past five years, compared to the health care holdings in our benchmark (and the biotech subsector within health care). It is a quick illustration of a meaningful driver of our performance: The biotech subsector takes up more than a third of our benchmark’s health care allocation, but we largely avoid investing in biotech firms. That subsector’s weak performance over the past five years dragged on the benchmark’s returns, but had little impact on our portfolio.

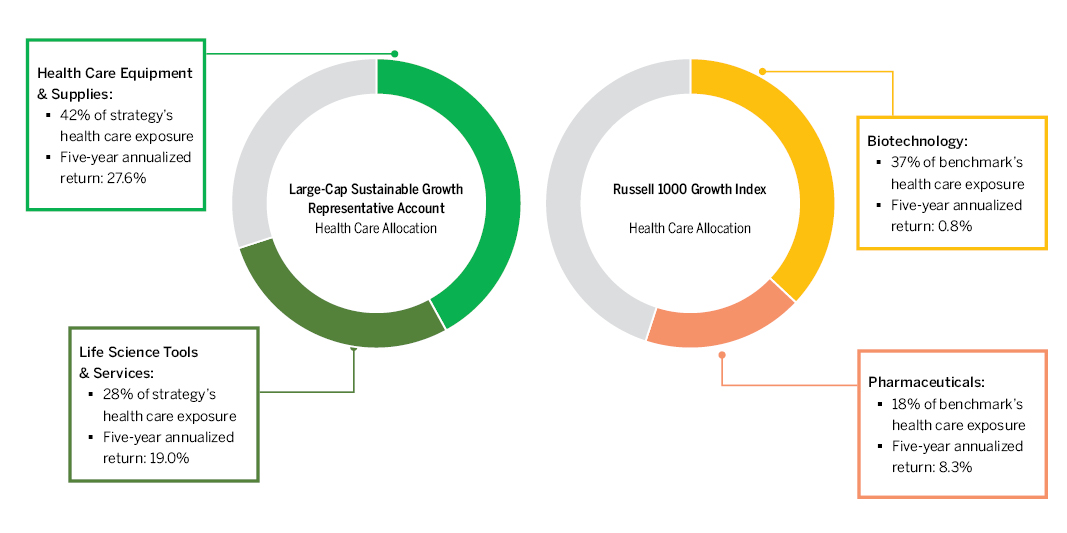

We can take this sector analysis further; the chart on the next page illustrates the breakdown of our health care holdings (in other words, our average weightings in various health care subsectors over time), vs. our benchmark. To be clear, we do not aim our investment at particular sectors or subsectors. But our criteria often lead us to specific areas of the economy where businesses are less subject to exogenous risk.

DISAGREEMENT CAN BE HEALTHY

Our strategy’s investments in the health care sector historically have looked very different from the makeup of the health care holdings in our benchmark. We have had minimal exposure to the risks in the pharma and biotech sectors, and instead have invested most of our capital with companies focused on devices, technologies and services that seek to improve the effectiveness of health care delivery in a measurable way. These choices have generally benefited our overall portfolio returns over the past five years.

Average Health Care Subsector Weightings and Gross Returns, Five-Year Lookback (9/30/2014-9/30/2019)

Source: Bloomberg. The portfolio information provided is based on a representative Large-Cap Sustainable Growth account and is provided as supplemental information. Subsector return figures provided above reflect the aggregated returns of the relevant equity holdings in the representative account portfolio and the benchmark, due to price movements and dividend payments or other sources of income, and exclude cash. Sector allocation data reflects average monthly exposure over the five-year period ended Sep. 30, 2019, and excludes cash and cash equivalents. Sectors and subsectors are based on the Global Industry Classification Standard (GICS®) classification system. Please see disclosure statements at the end of this presentation for the complete Large-Cap Sustainable Growth GIPS-compliant disclosure.

To be sure, our relative avoidance of the pharma and biotech subsectors has hurt us at times during our history when those sectors were outperforming. We can be fairly certain that we will be out of step again at some point in the future when momentum develops behind these and other segments of the health care industry. Cutting-edge drug research continues to produce some truly amazing discoveries, but we find it challenging to base an investment thesis on events that hinge on binary outcomes like regulatory approvals or litigation results. We prefer to invest where we have greater visibility over longer periods of time, and we believe that approach will serve us well.

Importantly, sector allocation is only part of the story—our stock selection has also benefited our returns. We are first and foremost bottom-up fundamental stock pickers; here we highlight several of our holdings that illustrate the kinds of opportunities we like to own:

- Edwards Lifesciences is a developer and manufacturer of technologies used to treat structural heart disease. The company’s transcatheter aortic valve replacement is less invasive than traditional open-heart surgery and is approved for patients deemed too high-risk for traditional surgery. This minimally invasive surgery technology effectively increases the probability of survival, reduces the length of hospital stays and readmission rates, and provides patients with a significantly higher quality of life post-surgery. A secondary (but still meaningful) benefit of Edwards’ technologies: reduced time in the hospital for patients means a reduction in waste generated during those hospital stays (an occupied hospital bed generates an average of thirteen pounds of medical waste per day, according to the Environmental Protection Agency). Edwards has been one of our stronger performers over the past year or so, and we believe it has a strong competitive position and the ability to maintain its leadership in its market for some time to come.

- We view Illumina as a great example of a business model that is on the right side of a health care sector risk, namely drug pricing and regulation. For a number of years, advances in genomic sequencing have led to incredibly effective drug treatments for small, targeted groups of patients; because of the smaller size of the patient audience for these targeted treatments, prices often have been extremely high. However, costs are gradually coming down in a number of cases, and insurance plans are beginning to cover these treatments thanks in no small part to companies like Illumina who are enabling more effective genomic research. Illumina offers a wide range of tools for large-scale analysis of genetic variation and function. We believe that regardless of the debate over drug pricing, Illumina is in an excellent position because its tools will always be in demand from health care firms who want to improve their research processes. Our investment in Illumina is, we hope, still in its early innings—it has not yet generated the returns for us that we believe it can earn over the coming years.

- In our view, Danaher has an especially interesting position in the health care market, due to its leadership position in bioprocessing workflow solutions. As we have noted, biotechnology stocks are volatile, but we believe that the sector offers undeniable growth potential over the next several years, driven by multiple secular tailwinds such as increasing penetration of existing drugs in high-growth markets like China, a rich development pipeline of new drugs and the rise of biosimilar drugs. To meet this demand, many companies are making large investments in bioprocessing equity and manufacturing infrastructure, and we believe that Danaher is poised to be a prime beneficiary of this industry-wide investment activity. As a result, by owning Danaher we believe that we can benefit from the growth of the biotechnology sector, without becoming unduly exposed to the pricing and regulatory risks endemic to the industry.

As a final note, we should mention that a number of our successful investments are not in the health care sector, but their growth has been partly propelled by health care drivers. When we think about the challenges and opportunities in health care, we try not to limit our thinking to the companies that are nominally “in” the health care sector according to GICS or any other classification system. For example, Fortive is the “other half” of Danaher, formed when Danaher divided its portfolio into two businesses. Danaher is now classified as a health care company, and Fortive as an industrial firm, but a variety of Fortive’s solutions are still aimed at the health care industry. Earlier this year, Fortive acquired Advanced Sterilization Products from Johnson & Johnson, giving it a leading position in sterilization and disinfection technology. These products and services help health care customers combat one of the leading causes of hospital readmissions.

Sustainability is complicated; making progress in one sector generally requires contributions from many other corners of the economy. We are finding companies across the entire equity universe that are driving innovation and value in the health care arena, and we will continue to explore the investment opportunities those companies create. ![]()

Click here to view Large-Cap Sustainable Growth Composite Disclosures

The views expressed are those of Brown Advisory as of the date referenced and are subject to change at any time based on market or other conditions. These views are not intended to be and should not be relied upon as investment advice and are not intended to be a forecast of future events or a guarantee of future results. Past performance is not a guarantee of future performance and you may not get back the amount invested.

Any business or tax discussion contained in this communication is not intended as a thorough, in-depth analysis of specific issues. The information provided in this material is not intended to be and should not be considered to be a recommendation or suggestion to engage in or refrain from a particular course of action or to make or hold a particular investment or pursue a particular investment strategy, including whether or not to buy, sell, or hold any of the securities mentioned. It should not be assumed that investments in such securities have been or will be profitable. To the extent specific securities are mentioned, they have been selected by the author on an objective basis to illustrate views expressed in the commentary and do not represent all of the securities purchased, sold or recommended for advisory clients. The information contained herein has been prepared from sources believed reliable but is not guaranteed by us as to its timeliness or accuracy, and is not a complete summary or statement of all available data. This piece is intended solely for our clients and prospective clients, is for informational purposes only, and is not individually tailored for or directed to any particular client or prospective client.

The S&P 500 Index is a capitalization-weighted index of 500 stocks that is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. Standard & Poor’s, S&P®, and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”), a subsidiary of S&P Global Inc.

Global Industry Classification Standard (GICS®) and “GICS” are service makers/trademarks of MSCI and Standard & Poor’s.

BLOOMBERG, is a trademark and service mark of Bloomberg Finance L.P., a Delaware limited partnership, or its subsidiaries.